Home » Buying and selling an apartment » Marriage agreement when buying an apartment with a mortgage

1

A mortgage has been and remains for many people one of the few ways to acquire their own home with minimal effort. Most often, young families plan to purchase an apartment, but due to the nature of joint ownership, it is most difficult for them to obtain such a loan on optimal terms. In many cases, banks offer (and sometimes require) a prenuptial agreement (also known as a prenuptial agreement). Why is this necessary and how it will help in obtaining a mortgage loan - read this article.

What is a prenuptial agreement?

A prenuptial agreement is an agreement that is concluded before the registration of marriage or during the period of marriage. It contains conditions relating to the property and financial aspects of family life.

The contract allows you to change the regime of joint ownership. A husband and wife can agree that all or only part of the property acquired during marriage goes to the one who financed the purchase upon divorce. They also have the right to immediately allocate shares to the property, which will not necessarily be equal.

The agreement is made only in writing. To give it legal force, it must be certified by a notary.

In addition to property, spouses can share debts. Therefore, a marriage contract is relevant when purchasing an apartment with a mortgage.

Useful video

Check out the lawyer's recommendations in the video below:

Notarization of the transaction between spouses regarding the registration of a marriage contract is mandatory. The cost of services for preparing contracts for individual offices, regardless of public or private status, varies.

Law firms replace busy notary offices at the project preparation stage; there is also the option of preparing a contract yourself. However, to give the document legal force, you need to visit a notary.

Why do you need a prenuptial agreement when buying an apartment with a mortgage?

Most often, banks insist on concluding an agreement. When issuing a loan to purchase a home, it is stipulated that the property will be pledged to the lender. He bears the risk of non-payment of the loan in the event of divorce and division of joint property.

If the borrower is one of the spouses, the contract allows for the establishment of separate ownership of the mortgaged apartment. After the divorce, the apartment and debts will pass to the borrower.

Situations in which it is advisable to sign an agreement between spouses are varied. Let's name some of them:

- spouses have different income levels;

- the husband or wife is in arrears on their debts;

- the bank refused to issue a mortgage loan because it doubted the creditworthiness of one of the spouses;

- husband or wife does not agree to a mortgage loan;

- one of the spouses does not have official employment and cannot confirm income;

- the mortgaged apartment was purchased before the marriage was registered;

- one of the spouses does not have Russian citizenship;

- the husband or wife has a criminal record;

- real estate is purchased with the money of the parents of one of the spouses;

- one of the borrowers avoids paying the mortgage loan;

- after a divorce, the loan debt is divided.

Thus, a prenuptial agreement for a mortgage is a way to protect the most financially vulnerable spouse and the credit institution that issued the loan from financial risks.

Disadvantages and risks when drawing up a prenuptial agreement for a mortgage loan

However, using a prenuptial agreement for a mortgage has a number of disadvantages:

- One spouse will be forced to take personal responsibility for paying off the mortgage.

- When calculating the maximum available amount, the financial institution will take into account the income of only one person. As a result, the available limit for purchasing a property may be significantly lower.

- If a citizen’s income is low, the likelihood of loan refusal increases.

The main risk of concluding a prenuptial agreement for a husband and wife is considered to be the likelihood of drastic changes in the life of the family. The income of one spouse may increase significantly. As a result, he begins to earn more than his husband or wife. A number of people believe that in this case the spouse should increase the costs of the mortgage. However, adjusting the prenuptial agreement with a mortgage is problematic. Amendments or termination of the spouses’ agreement for a mortgage loan is possible only by mutual consent of the parties (Articles 43 and 44 of the RF IC).

Features of a prenuptial agreement for a mortgage

When purchasing an apartment with a mortgage, in addition to property rights to the property, obligations arise to repay the loan. Therefore, when concluding a contract between spouses, you need to pay attention to some nuances.

Before marriage

An apartment purchased with a mortgage before marriage belongs solely to the person who bought it. If the second spouse helped pay the loan, this does not give him the right to a share in the property. In the event of a divorce without the consent of the borrower, he will receive nothing.

In such a situation, it is recommended to sign a prenuptial agreement with conditions governing the repayment of the housing loan taken out before marriage. It is also necessary to clearly delineate the rights of the parties to residential real estate.

The contract may include the following conditions:

- The borrower repays the loan independently; after the divorce, the apartment remains his property.

- Spouses jointly repay the loan debt; in the event of divorce, each of them receives a share in the right to residential real estate.

In the first case, the agreement protects the property interests of the spouse, who independently bore the costs of the mortgage loan. In the second , it insures the financial risks of the spouse who provides assistance in repaying the debt.

During the period of marriage

Most often, a prenuptial agreement is signed during marriage, when the family buys an apartment with a mortgage. When accepting the application, the bank employee asks whether the spouses signed the agreement or not.

If a community property regime is established, the bank will involve the husband and wife as co-borrowers. In case of a separate regime, the loan will be given to one of them. Ownership of the property will also be registered in his name.

After divorce

You can conclude a contract before registering a relationship or during marriage. After a divorce, you cannot sign an agreement. In this case, when dividing property, the rules of joint ownership of property apply. Therefore, the spouses will have to defend their interests in court or try to come to an agreement with each other.

Buying an apartment using maternity capital

Many families purchase housing on credit with maternity capital. It is used as a down payment or used to pay off a mortgage.

In accordance with the requirements of the law, real estate is registered as shared ownership. Shares are distributed between parents and children.

It is not possible to re-register housing in the name of one of the spouses. If the borrower is one spouse, the marriage agreement specifies the share of the husband and wife. Shares registered in the name of children are not subject to division.

Property acquired before marriage

In Art. 34 of the Family Code of the Russian Federation states that property that spouses acquired during marriage is their joint property. Based on this, we can conclude that there is no point in concluding a contract that would include real estate acquired before the formalization of family relations.

But this conclusion will not be entirely correct. Why?

Example: a man purchased an apartment with a mortgage, did not have time to repay the loan and got married. The real estate purchase and sale agreement, in this case, will be signed before marriage. But payments to the bank will be made during the existence of the family union. By default - from the common funds of the husband and wife. This means that the wife, in the event of, for example, divorce, will have the right to demand the allocation of a share in her favor in the specified property.

To prevent such a right from arising, it is necessary to conclude a marriage contract, which would indicate that loan payments will be made from the husband’s personal funds. Accordingly, the apartment will be considered only his personal property.

We can talk about other cases when it is worth talking about an apartment purchased before marriage in a marriage contract.

Another example: before going to the registry office, a man had a modest one-room apartment, inherited from his grandmother. During the marriage, the couple made expensive repairs to it:

- replaced wooden windows with plastic ones;

- they insulated the balcony, turning it, in fact, into another room;

- replaced all the doors;

- laid laminate;

- updated plumbing and so on.

In total, an amount equal to almost half the value of the property was spent. According to the norms of the Civil Code of the Russian Federation, if a person who is not the owner of the property has made significant inseparable improvements to the property, he has the right to demand the allocation of a share in the property. At a minimum, you can count on monetary compensation. Art. also speaks about this. 37 RF IC.

In this case, in the absence of a contract, it can be considered that the improvements to the property were made using funds acquired during the marriage. Accordingly, if an amount equal to half the cost of the apartment was spent, then the spouse has the right to demand the allocation in her favor of 1/4 of the share in the ownership of the real estate.

To prevent such a right from arising, it is necessary to conclude an agreement in which it will be stipulated, for example, that the improvements were carried out only at the expense of the husband’s personal funds.

Thus, in most cases, it makes no sense to conclude a prenuptial agreement for an apartment purchased during marriage. But there are certain exceptions to this rule.

Pros and cons of a prenuptial agreement for a mortgage loan

A prenuptial agreement for a mortgage has its pros and cons .

advantages can be mentioned :

- delineates the rights of husbands and wives to housing;

- determines the scope of the spouses’ obligations under the mortgage loan;

- insures the financial risks of the parties in case of unequal financial situation;

- makes it possible to get a loan even in case of objections from the second spouse.

Many citizens believe that love and mercantile calculation are incompatible concepts. Therefore, they are in no hurry to conclude a marriage contract. Most often, the agreement is signed at the insistence of the bank.

The procedure has some disadvantages :

- high cost of notary services;

- if new legal requirements are introduced, changes must be made to the agreement, otherwise it will be invalid;

- it is difficult to foresee all controversial situations;

- the contract comes into force only after the marriage is registered.

If, under the terms of the marriage contract, the apartment goes to one owner, the bank may provide a loan on less favorable terms. If there is no co-borrower, only the income of one spouse is taken into account, so the loan is issued in a smaller amount.

How to draw up a marriage contract for a mortgaged apartment?

When drawing up a marriage contract, you must be guided by the requirements of Chapter 8 of the RF IC.

It is necessary to pay attention to the following points:

- the contract is signed by legally capable citizens who have reached the age of majority;

- to give legal force, the document is certified by a notary;

- the text of the agreement must be clear and precise, without corrections, abbreviations are not allowed, digital designations are written in words;

- You cannot sign a document if the parties are in a civil marriage and do not intend to register the relationship;

- the document is signed personally by the husband and wife.

After deciding on a joint mortgage, you need to decide on a credit institution. Then a contract is drawn up. If it is difficult to do this on your own, we recommend contacting a professional family law lawyer. After signing the contract, it is certified by a notary.

Sample marriage contract for a mortgage and its contents

The prenuptial agreement must contain terms regarding the mortgaged apartment.

The standard agreement includes the following items:

- date of signing the contract;

- information about husband and wife (full name, addresses, passport details);

- information about marriage registration;

- information about residential real estate (cadastral number, area, number of rooms, number of floors);

- the procedure for dividing property during divorce;

- how shares will be redistributed in the event of children;

- information about the credit institution that issued the loan;

- who is the mortgage borrower;

- who pays the down payment and in what amount;

- how the loan debt will be divided in the event of divorce;

- liability for violation of agreements;

- duration of the agreement;

- signatures of the parties.

The parties have the right to include any provisions that do not contradict the law. Exceptions include personal relationships, obligations to children, and extremely unfavorable conditions.

Certification from a notary

After signing the agreement, you must visit the notary's office.

Along with the contract the following are provided:

- participants' passports;

- certificate of registration of marriage relations;

- package of documentation for residential real estate (loan agreement, purchase and sale agreement, cadastral passport);

- receipt of payment of state duty.

According to Article 333.24 of the Tax Code of the Russian Federation, a state duty in the amount of 500 rubles is charged for certifying a marriage contract. This price includes services for:

- checking the agreement for compliance with legal requirements and authenticity;

- identification of participants by their identity cards;

- establishing the actual existence of property;

- counseling for spouses.

It happens that spouses turn to a notary office to draw up an agreement. This service is not included in the state fee. The specialist advises the husband and wife on each provision of the contract, draws up a document taking into account their wishes, collects and checks all the necessary documentation. The cost of a marriage contract from a notary on average across regions is 5,000 rubles.

Concept and application

A marriage contract is an official document that is used to resolve issues related to the family relations of spouses.

Its concept is enshrined in family law, namely in Art. 40 IC RF.

In accordance with this article, a marriage contract is a document that fully regulates all relations (both property and non-property) between spouses.

It can be formalized both before the official registration of marriage, and in

during the entire period of its validity, already between legal spouses. Its main goal is to regulate relations between them on all possible controversial issues and resolve them quickly and beneficially for both parties.

The contract extends to the entire period of the marriage and is terminated only in the event of its dissolution or invalidation. However, in some cases, its effect continues after the divorce, if the document includes some obligations of the parties after the dissolution of the marriage.

It is worth noting that the document is most widespread in Western countries, where it is almost always drawn up when citizens get married.

In Russia, this agreement is not yet popular and is concluded only in alliances whose parties are very wealthy and famous people.

It has also become widespread in situations related to obtaining a mortgage. Since this is a long-term transaction and its value is usually very large, many difficulties may arise during its operation. In particular, some of them are related to the divorce of spouses and the division of property purchased in this way. To ensure that these issues are resolved as quickly and beneficially as possible for the parties, a prenuptial agreement is used.

Is it possible to terminate a marriage contract if the apartment is under mortgage?

By agreement of the parties, the contract may be terminated. In the future, the division of property is carried out according to the general rules of the RF IC.

It happens that a spouse is forced to terminate a contract unilaterally. This is possible if:

- the second spouse died;

- the party to the agreement is declared incompetent;

- husband or wife has gone missing.

In the first case, a death certificate will be required, in the rest - a court decision.

Something to remember! The borrower must notify the bank that the agreement has been terminated. Otherwise, he will be personally responsible to the credit institution, regardless of what conditions were contained in the contract.

After informing the bank about the termination of the contract, it has the right to demand:

- make changes to the loan agreement;

- repay the debt ahead of schedule if the financial situation of the creditor has worsened.

If you have any doubts about terminating your prenuptial agreement, it is recommended that you consult with a qualified attorney.

How can a husband or wife get a mortgage loan while married?

A spouse who has decided to take on the mortgage obligations solely on himself is required to prepare a package of papers.

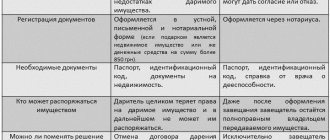

Required documents

To apply for a mortgage loan, you need to bring the following documents to the bank:

- passport confirming Russian citizenship;

- documents confirming the availability of residence registration;

- work book;

- TIN/SNILS;

- Form 2-NDFL, some organizations request certificates based on the bank model;

- other documents reflecting the borrower’s income level;

- an extract from a bank account containing an amount sufficient to pay the down payment;

- Individual entrepreneurs are required to provide a tax return;

- marriage certificate;

- a marriage contract certified by a notary office, which describes in detail the rights of the spouses to the collateral property;

- consent of the spouse not participating in the mortgage to purchase real estate;

- driver's license or certificate from the PND.

If the application is approved, you will need to collect documentation for the purchased living space:

- seller's identity document;

- an extract from Rosreestr stating that there are no encumbrances;

- document confirming ownership;

- a purchase and sale agreement or other paper that serves as the basis for the acquisition of ownership rights;

- consent to the sale of real estate from the husband or wife of the seller;

- an extract from the house register, where there should be no people registered in the apartment for sale;

- documents for the territory;

- technical certificate.

Since 2020, the cadastral passport for the purchase and sale of an apartment is replaced by an extract from Rosreestr.

Features of drawing up a marriage contract

As stated in paragraph 2 of Art. 41 of the RF IC, a marriage contract is drawn up in a notary’s office in the presence of both spouses. This document defines the property regime of the parties.

If the contract is drawn up correctly, it should contain the following points:

- Who will own the property?

- Who is required to pay the down payment?

- Who will take on the responsibility of paying monthly payments?

- The source of funds from which money will be drawn each month to pay your mortgage.

- Name of the bank issuing the loan.

- Is it possible to provide common property as collateral?

- Will a separate property regime be established? If the answer is positive, only the spouse acting as the borrower will become the owner of the apartment, and the other party will not be able to claim it in the event of a divorce.

- An explanation that all obligations regarding the payment of the collateral are assumed by the borrower, and the second spouse does not enter into any relationship with the lender.

We do not recommend completing the documents yourself. Save time - contact our lawyers by phone:

+7 (499) 938-90-71Moscow

Features of drawing up an application

An application for mortgage lending is drawn up according to a generally accepted template, but it must be submitted only on behalf of the borrower. The second spouse does not take part in filling out the application form, but his presence at the bank is still required. The application contains the following points:

- information about the applicant: full name, date of birth, passport details, gender, tax identification number;

- information about the change of full name;

- contacts: telephone, email;

- marital status: married;

- addresses of place of registration and residence;

- family composition, whether the spouse and children are dependent;

- availability of education;

- employment information;

- income level;

- property owned by the borrower.

Step by step procedure

To obtain a mortgage loan you must complete the following steps:

- Spouses signing a marriage contract.

- Filing an application. Many banks offer to submit an application online, but if the procedure differs from the standard one, as when applying for a loan for one spouse, it is advisable to come to the branch in person.

- Submitting the application and accompanying documents to the bank.

- Mortgage approval

- Selection of real estate.

- Collection of documentation for the apartment.

- Calling experts to evaluate the purchased property, submitting the results of the examination to the bank.

- If the object is approved, the date for concluding the loan agreement is discussed.

- Signing an agreement to insure the apartment, as well as the life and health of the borrower.

- Concluding an agreement with the bank on obtaining a mortgage loan.

- Execution of a purchase and sale agreement, transfer of a pre-agreed amount of finance, registration of property rights.

Can they refuse and why, how can I increase my chances of approval?

Most often, the reason for refusal to issue a mortgage loan is the low income of a potential client. The monthly payment should not be more than 45% of the official part of the salary. Otherwise, the borrower is considered unreliable.

To increase the chances of approval, you can attract guarantors or other co-borrowers, for example: sisters, brothers, parents. Another option is to offer the bank property as additional collateral.

Is it possible to challenge the transaction?

If an agreement violates the rights of one of the parties, it can be challenged in court. A positive decision is possible only if there are compelling reasons established by the Civil Code of the Russian Federation.

A contract is considered invalid in the following cases:

- lack of notarization:

- signing by an incapacitated person;

- concluding an agreement under the influence of violence, threats, deception, misconception;

- the provisions of the contract infringe on the rights of the husband or wife.

If a party decides to appeal the contract in court, the credit institution must be notified about this.