Not all people retiring know exactly how pensions are calculated. For some, it seems quite complicated, which is why they do not dive into the details, but trust the Pension Fund of the Russian Federation and simply receive the amount assigned to them. However, such knowledge will be quite useful for every person.

How to calculate your pension?

In this article we will talk about how to calculate a pension, what parts it consists of and what ways you can increase it.

Components of pension payments

Pension payments consist of three parts: fixed, insurance payments, depending on the age of the citizen and accumulated.

Fixed part

All citizens receiving insurance pension payments have a fixed part of the pension fund included in them. This component is constant and does not depend on the length of service of a citizen of the Russian Federation. The size of the fixed part is assigned by the state and is revised every year due to changes in pricing policy in the Russian Federation. From January 1, 2020, the PV indicator was changed to 7.05% - this is more than the inflation index in 2021 (according to Rosstat - 4.3%).

Note! The amount of the fixed part for 2020 is 5334.19 rubles (the increase compared to 2021 is 351.29 rubles).

All citizens are obligated to pay the pension fund

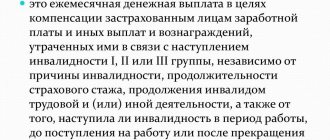

Note that the legislation regulates the size of the PV for old-age pension compensation; based on these data, the PV for other types of pension payments is regulated. The amount of pension compensation should be revised if a citizen is assigned a disability or as a result of the death of the breadwinner. Let's consider the PV indicator used in 2021 for people of retirement age who have completed their working career:

- For persons with disabilities of group 1, the PV will consist of double the cost of the PV for old age, namely 10,668.38 rubles.

- For persons with disabilities of group 2, the PV will be equal to the PV for old age, namely 5334.19 rubles. in 2021

- For persons with group 3 disability and in the event of the loss of the main breadwinner of the family, the PV is equal to 1⁄2 of the constant amount paid for old age, 2667.10 rubles, respectively.

The amount of pension compensation is revised if a citizen is assigned disability

For a Russian of retirement age who continues to actively work, the amount of the PV is not subject to indexation as long as he works. In other words, the fixed part remains unchanged until the person leaves. Each citizen will be assigned the amount of fixed compensation that was established during the year of the person’s leave for labor rest. You can analyze this data using the table.

| Time for registration of the insurance share of pension payments | PV value, rub. |

| Until January 1, 2016 | 4383.59 |

| From 1.02.2016 | 4558.93 |

| From 1.02.2017 | 4805.11 |

| From January 1, 2018 | 4982.9 |

| From January 1, 2019 | 5334.19 |

Insurance part

This is an amount paid to a person monthly in order to replace the income that the citizen could receive while continuing his work activity.

What criteria are important to meet to receive such compensation? These include age, type of work activity, its duration and the number of pension points at the bottom level. It is advisable to hope for insurance compensation for old age when the following requirements are simultaneously met:

- The 61-year-old threshold for the stronger sex and 56-year-old for the weaker sex have been reached. Since the beginning of 2021, the Russian Federation has begun to gradually raise the retirement age; it is now 65 and 60 years, respectively. For citizens who were supposed to retire in 2021, there will be more favorable conditions: they will need to work an additional 6 months.

- However, there is a category of people who will not be affected by the changes in the pension reform – this includes beneficiaries. Municipal government employees and citizens in public service will have to extend their careers. The age limit for taking a working holiday will also rise for officials from 2021: from 2021 it will be 56.5 and 61.5 years for women and men, respectively.

- Official work experience is at most 10 years (important information for 2021 - this figure will increase after a certain period).

- The accumulation of pension points has reached a minimum level of 16.2 (important for 2021, the indicator will increase over time). This indicator is the sum of the total insurance payments made during the working period.

Also, if certain conditions are detected, citizens are paid the insurance portion

If a citizen did not manage to work the required number of years or did not achieve the minimum pension points, then he is deprived of the opportunity to pay a guaranteed share of pension compensation.

Note! Taking a well-deserved rest ahead of schedule (for example, if a citizen worked in conditions harmful to health or harsh climatic conditions, or carried out teaching or medical activities) will not be possible if the required number of years has not been worked and there is no documentation recording income and the nature of work duties.

The insured pension consists of the following shares:

- Share of guaranteed compensation earned before 2002.

- The share of guaranteed compensation, which was calculated from 2002 to 2014.

- Share of guaranteed compensation earned after 2015.

- The share of guaranteed compensation added for other (not related to insurance) time.

The insurance part of the pension is paid if the person has accumulated the required number of pension points

Important! From 2015 to the present, pension funds for any period of old age that are under state insurance are influenced by the individual pension coefficient (IPC), calculated in points. If you know its value, then it is easy to calculate the amount of pension funding in rubles.

The guaranteed share of pension compensation in rubles is equal to the IPC multiplied by the value of the pension point on the date of determination of the insured pension compensation, plus a constant payment on the date of determination of the insured pension compensation.

In 2021, the formula takes the following form:

Insured pension compensation in rubles = IPC × 87.24 rubles + 5,334.19 rubles

Insurance pension calculator

Go to calculations

Cumulative part

The cumulative share of the pension is money made up of insurance contributions that the employer transfers monthly to the personal account of his employee. If a person has worked the required period and decided to retire, he has the right to count on receiving a monthly portion of the accumulated amount or receive the entire amount once in full.

The funded part of the pension can be received as a lump sum or monthly

Only citizens who have officially completed the insurance procedure and have the right to payment of a guaranteed share of pension savings are eligible for accumulative pension compensation.

The following persons apply for the issuance of a funded share of pension finance:

- Citizens born in 1967 and later who are officially employed, for whom the employer made insurance contributions, due to which finances are generated for the accumulative share of the pension capital.

- Males born in 1953-1966, and women born in 1957-1966, for whom employers made insurance contributions from 2002 to 2004.

- Female representatives have the opportunity to take advantage of the allocation of maternity capital to organize a funded portion of their own pension in the future.

- Citizens involved in the State Pension Financing Program.

A certain category of persons may qualify for the funded part of the pension

It is easy to calculate the cumulative share using the formula:

Accumulation share = total amount of pension savings / probable period of payment of accumulated pension compensation

The expected period for payment of the accumulative share of pension savings increases annually by 6 months. In 2021, this standard is equal to 246 months, and in 2012 – 252 months.

Note! In order to inform about the volume of the cumulative share of pension savings, you can visit the MFC or the Pension Fund. A convenient option would be to use the official website of the Pension Fund of Russia.

You can check the amount of the funded part of your pension on the Pension Fund website

Size of the base for certain categories of the population

The amount of the basic component of the pension depends on many factors, so its size is calculated taking into account the category of citizens applying for benefits:

- How much is it today (minimum) - as a result of indexation in 2021, the basic component of the pension was adopted in the amount of 4982.9 rubles, which is equivalent to the minimum pension in the Russian Federation.

- For law enforcement officers , military personnel are not eligible for a basic pension, since the calculation of pension benefits is carried out in a slightly different way than for civilians, taking into account allowances, length of service and the amount of monthly allowance. Their pension is indexed and increases annually. The minimum pension amount cannot be lower than the basic component at the time the serviceman receives it.

- For disability - the size of the base depends on several criteria, including the disability group. The minimum is 9965.80 rubles, and if there are dependents on support, it increases to 14948.71, taking into account the number of dependents. If a disabled person is not able to care for himself, the minimum amount increases to 21,622.98 rubles, and if he works in the Far North - 14,948.71 rubles.

- In the regions of the Far North , difficult working conditions guarantee an increase in the basic component of the pension, taking into account length of service. The minimum amount is 7474.35 rubles, and if there are dependents, this amount increases by 30% for each dependent.

- If there are dependent dependents , the pension supplement is provided for a maximum of 3 people and depends on which category the recipient belongs to. For residents of the Far North, the premium is 50%, for regions equated to the North - 30%, in the absence of any benefits or subsidies - 50%.

- For officials - fixed pension payments are due to a civil servant only if he takes out an old-age pension. In other cases, pension calculation is carried out individually, taking into account the position held, salary and benefits.

- For working pensioners - if the pensioner continues to work, the law secures his right to receive a basic pension. However, this amount is not subject to indexation. Only after full retirement will its amount be recalculated taking into account the minimum in the region.

- For veterans of the war in Afghanistan , the base is calculated upon reaching retirement age (old age) or disability. In other cases, the size of the pension depends on the position held, as well as benefits provided by the state.

- For individual entrepreneurs - if an individual entrepreneur makes contributions to a pension fund, upon reaching retirement age he can qualify to receive the basic component of the pension.

READ How to calculate vacation pay: how to calculate, average minimum wage earnings in 2021, percentage of vacation pay from salary

What measures need to be taken now to ensure larger pension payments in the future?

Official employment

If the amount of earnings officially recorded is commensurate with the minimum amount of wages, and additional payment is made through a card or in another way, then you should take into account that the accumulation of pension points is made only from the minimum amount. Consequently, old-age pension payments will be very modest.

The size of the pension is influenced by the period in which the person was officially employed

Try to get the maximum possible salary

It is worth remembering: the higher the official earnings today, the more pleasant pension compensation will be in old age. The higher the salary, the higher the contributions for pensions in the future.

In 2021, the highest pension score that can be earned is 9.13. To reach this mark, the officially registered salary must be 87,500 rubles, excluding tax deductions. A good incentive to move forward.

The higher the salary, the larger the pension will be

Pension for those born before 1967

The Russian government is actively pursuing pension reform in 2021. The pension calculation for those born before 1967 consists of three parts. This:

- base share;

- Cumulative share;

- insurance

Basic part

Basic is a fixed compensation that every person who has reached old age receives, regardless of length of service. From January 1, 2002, the final base rate was set at 450 rubles per month. This amount is due to all citizens who have reached old age and have worked for more than 5 years. Its size is affected by a person's age.

Cumulative part of pension provision

This share is available only to those citizens who were born before 1967 and are participants in the OPS. It is formed if in the period from 2002 to 2004. The employer paid monthly insurance premiums for the funded share of labor activity in the amount of 6% of wages. It is formed on a voluntary basis for participants in the State Pension Co-financing Program and persons who allocated funds from maternity (family) capital to form the funded part. The total amount going to the savings share should not exceed 463,000 rubles per year.

Based on the federal decree, paragraph 11 of Art. 31 “On investing funds to finance the funded part of labor benefits in the Russian Federation”, insured persons born before 1967, who have entered into an agreement on compulsory pension insurance and who have applied to transfer to a non-state fund (NPF), submit an application for refusal to finance the funded fund part and direction to finance the insurance part in the amount of 6 percent of the individual part of the insurance premium tariff.

Citizens can find out about their savings in the Pension Fund of the Russian Federation by writing an application in the prescribed form. Payments of state support, in accordance with clause 2 of Art. 217 of the Tax Code of the Russian Federation are not subject to taxation and are not taken into account in calculations of personal income tax, with the exception of payments if the individual has voluntary insurance of the funded part.

Insurance pension

It includes all work experience accumulated by 2002, the amount of wages and a special coefficient. Let us analyze the methodology for calculating the insurance share, which should be calculated according to the following algorithm:

- SP = PB * CB * PK1 + FV * PK2, where: SP is the amount of funds calculated to pay the insurance benefit;

- PB – points accumulated over time;

- Central Bank – the price for 1 point established at the time of calculation;

- PC1 and PC2 are increasing bonus coefficients for retirement at a later period;

- FV – fixed amount

- How to make paste from flour

- How to choose a grill pan

- How to make pancakes

How is it possible to receive an accumulative share of pension capital?

There are three options for obtaining this finance:

- option for a one-time financial payment in the case where the accumulated pension is 5% or less of the total funds of insured and accumulated pension savings;

- option for urgent issuance of pension finance. This applies to participants in the State Pension Co-financing Program and mothers who decide to create a financial cushion for pensions from maternity capital;

- option for lifetime payment of a funded share. Its amount is determined by determining the ratio of the finances of pension savings to the expected time of payment of the funded share. The latter indicator is regulated annually by federal law. In 2020 it was 252 months.

Time to pay out the accumulative share in 2021 – 252 months

Important! Let’s assume that the cumulative share of a citizen’s pension has reached 280 thousand rubles. You need to divide this figure by 246 months, as a result you will know the amount of the funded share payment that will be made monthly. In this particular case, it is equal to 1138.21 rubles.

Required experience and coefficient for registration

To receive an insurance pension, a citizen must have at least 10 years of work experience. This figure will increase from 2019 to 2024 until it reaches 15 years. The insurance period is determined depending on the number of years worked, which are reflected in the individual accounting information. The last accounting date is the day you contact the fund to process payments.

To receive insurance payment, you will need to provide proof of work experience using a work book and certificates from employers. In some cases, citizens have to prove their experience in court, since the Pension Fund of the Russian Federation does not agree to take into account the time worked.

The length of service takes into account not only the time that was directly worked, but also some other periods of life.

Total work experience is accumulated in the following cases:

- dependent care;

- Military service;

- child care up to one and a half years old;

- time spent by military wives in closed areas;

- unemployment with benefits;

- serving a sentence in correctional institutions if the person turns out to be innocent.

The reform entails an increase in the required minimum pension coefficient. If in 2021 it is 16.2, then in 2021 it should be 18.6. The individual coefficient reflects the amount of funds transferred to the Pension Fund for the period of work and other types of work experience. The indicator directly affects the size of the final payment.

To start receiving contributions, a citizen must submit a corresponding application to the Pension Fund. To accept it, you must meet the conditions set at the state level. A person has the right to apply immediately upon reaching the required age or later.

How to determine the individual pension coefficient?

This is a very popular question that requires careful clarification.

The general IPC is a set of four IPCs, which are determined for a certain time period when the insurance part of the pension payment begins to be accrued.

IPC = IPC before 2002 + IPC for 2002–2014 + IPC after 2015 + IPC for other time periods.

The difficult thing is that the coefficient for different time periods has different calculations.

The total IPC is made up of four IPCs

IPC until 2002

The indicator of this period depends on three points:

- duration of labor activity until 2002;

- the average size of the legally established salary per month from 2000 to 2001 or any 5 years until January 1, 2002 (you need to select the most profitable indicator);

- duration of work activity until 1991.

How accurately the assessment will be made depends on the amount of pension compensation in rubles. There is a subtlety here: the Pension Fund does not have the full amount of data on citizens for the established time period. For this reason, the coefficient indicator in the online program will be approximate.

Note! If a citizen does not agree with this indicator, then he has the right to challenge it, but to do this he needs to recalculate everything himself and send supporting documentation to the Pension Fund.

The Pension Fund does not have complete data on the earnings of citizens before 2002, which is why the calculation is made approximately

IPC in the period 2002–2014.

The coefficient for this time period is influenced by the size of the pension capital, which consists of insurance payments made during this period. The number of months worked during this time does not matter, since the length of service is not taken into account for calculations.

The Pension Fund has information on Russians for 2002-2004, so there are practically no inaccuracies and errors compared to the first case. To facilitate calculations, it is convenient to use an online program.

The IPC in the period 2002-2014 consists of insurance payments made during this period

IPC after 2015

The size of the coefficient for this time period is influenced solely by the monetary indicator of insurance accruals that were transferred by the employee.

The accepted value of such contributions changes annually; accordingly, the coefficient must be recalculated every year. Then the obtained data is summarized.

If you do the calculations yourself, you can use simple formulas. They help you get reliable results:

IPC 2016 = average monthly salary in 2021 / 59,250 × 10;

The largest value is 7.39.

IPC 2017 = average monthly salary in 2021 / 66,333 × 10;

The largest value is 7.83.

IPC 2018 = average monthly salary in 2021 / 73,000 × 10;

The largest value is 8.26.

IPC 2019 = average monthly salary in 2021 / 85,083 × 10;

The largest value is 8.7.

IPC 2020 = labor income for 2021 until retirement × 0.16 /

184 000 × 10;

The largest value is 9.13.

The IPC after 2015 can be calculated using special formulas

IPC for another time

Other time periods include socially significant events that occurred in the life of a citizen, in particular, military service or the birth of a child. According to legislative act No. 400-FZ, each time period has its own special coefficient. For a parent who cared for the first child, or a man who served in the army, the IPC value is 1.8.

Note! For the parent who cared for the second child, the IPC value will be 3.6.

For parents and people who served in the army, there are also certain IPC values

The overall IPC indicator for other time periods is the sum of the coefficients for each time period taken separately. It is easy to calculate the total value of the IPC using a calculator.

How is the old age pension calculated in 2019?

The law says that in order to receive payments, a citizen must meet the following requirements:

- Age. Changes in 2021 have dramatically changed this figure and in 2021 the minimum age for men is 65 years and for women 60 years. But the law provides for categories that can receive assistance earlier. This applies to mothers of many children, medical workers, public transport drivers, disabled people, miners and people working in the Far North.

- Experience _ Now it must be at least nine years, but it is gradually increasing, and by 2024 it will be at least seven years.

- Points. A few years ago the points law was introduced. If there are not enough of them, then the payment will not be credited. But if there is a shortage, you can get them by paying a contribution to the Pension Fund. Today, to receive a pension, a person must have 11.4 points, but this figure is also increased every year.

Pension payments consist of a basic, funded and insurance part. The first part is a fixed payment established by the state, the second is the employer’s contribution, and the third is compensation for work activities.

Calculation algorithm

Today, citizens can find out the amount of payments using a calculation algorithm - you need to multiply the number of points by the cost of one point. The basic pension is added to this amount. As a result, the size assigned by the state appears.

Difficulties may arise when calculating pension points. It is also not easy to obtain information about the cost of a point. In 2021, a point cost 87 rubles. 24 kopecks, and the basic payment is 5334 rubles. 19 kopecks.

According to the accrual rules, the order will be as follows:

- A citizen must contact the pension fund and write an application for a pension. The form must be filled out on site or on the government services website.

- You also need to take your passport with you. This is necessary to confirm identity, age and citizenship. If there is no document, the application will not be accepted.

- Submit documents to confirm your experience. A work record book is not enough for this. You cannot do without orders, certificates, contracts and others. You need to collect everything.

- Information about the presence of dependents. This affects the payout amount. It may increase depending on the number of dependents.

- Bring your individual personal account insurance number card. If it is lost, it can be restored to the Pension Fund.

You also need to bring a certificate stating what your average monthly salary was over the last 5 years.

Attention! Those who have lost their certificate can contact their employer. By law he is obliged to provide it.

How to verify the reliability of an employer?

It is possible to find out the amount of insurance payments deducted by the employer, periods of work activity, places of employment and the number of pension points:

- on the website of the Pension Fund of Russia in the section “Electronic services and services of the Pension Fund of Russia” with further entry into the “Citizen’s Personal Account”;

- using the Unified Portal of State and Municipal Services;

- through the Pension Fund program for smartphones. It can be installed on iOS and Android platforms.

You can even check the amount of insurance payments through the Pension Fund program for smartphones

Deadlines for assigning insurance pensions in Russia

The law provides for the time frame within which an insurance pension can be assigned.

Let's consider when the old-age pension will be granted in 2021 and subsequent years.

| Year of entitlement to old-age insurance pension | Deadlines for assigning an old-age insurance pension |

| 2019 | Not earlier than 12 months from the date on which the right to an old-age insurance pension arises |

| 2020 | Not earlier than 24 months from the date on which the right to an old-age insurance pension arises |

| 2021 | Not earlier than 36 months from the date on which the right to an old-age insurance pension arises |

| 2022 | Not earlier than 48 months from the date on which the right to an old-age insurance pension arises |

| 2023 and beyond | Not earlier than 60 months from the date on which the right to an old-age insurance pension arises.” |

These deadlines are indicated in Appendix 7 to Federal Law No. 350.

What is the value of a pension point in 2020?

The decision on the value of a pension point for the purpose of assigning pension payments is regulated by the Government of the Russian Federation every year. Previously, indexing of its size was carried out every year from February 1, according to the new rule, this procedure will be carried out from January 1 in the period from 2021 to 2024. From January 2021, the pension coefficient was checked, its price was 87.24 rubles.

Note! This indicator will be used to calculate pension compensation in 2021.

The cost of one pension point in 2021 is 87.24 rubles.

For pensioners who decide to continue their careers, the value of one coefficient in 2021 will remain unchanged due to the moratorium on indexation of PV and SPK. One point for them will have a constant value when calculating pension payments in 2020.

Consider the table below.

| Date of registration of insurance pension | Cost of 1 pension coefficient, in rubles. |

| Until January 1, 2016 | 71.41 |

| From 1.02.2016 | 72.27 |

| From 1.02.2017 | 78.28 |

| From January 1, 2018 | 81.49 |

| From January 1, 2019 | 87.24 |

What parts does the old age pension consist of?

The old-age pension consists of two parts - the insurance part and the fixed payment.

Insurance part.

The size of the insurance portion is determined as the product of the individual pension coefficient (IPC) of a citizen and the cost of one pension point.

Individual pension coefficient (IPC)

is the current amount of pension points earned by the citizen. Every calendar year, insurance premiums paid by the employer in favor of its employee are recalculated into pension points.

Every year, the points are summed up and, accordingly, the current value of the IPC of the future pensioner is determined (the value of the IPC grows).

Pension point cost

is the price of one point expressed in rubles, set by the state annually. Until recently, the value of a pension point was set taking into account inflation of the previous year from February 1, and was updated from April 1.

The value of the pension point increased annually by no less than the annual increase in the price index.

Starting from 2021, the indexation procedure for determining the value of a pension point has been cancelled. Law 350-FZ approved the cost of one pension point for each year until 2024, inclusive. Every year from January 1, the cost of the point specified in Law 350-FZ will be established.

When assigning a pension to a future pensioner, his IPC (that is, the generated amount of pension points) is multiplied by the current value of one point and the result is the size of the insurance part of the insurance pension.

Fixed payment.

This is a certain amount in rubles, established as an additional payment to the insurance pension. This payment is received by all pensioners who are assigned an old-age insurance pension. The amount of this payment is set by the state annually.

Expert opinion

Mikhailov Konstantin Kirillovich

Lawyer with 7 years of experience. Specializes in the field of civil law. Legal expert.

The answer to the question of what the old-age insurance pension consists of is given above. The two components described above (IPC and fixed payment), which make up the pension, actually determine its size.

With more detailed information about the individual pension ratio

, as well as about

the fixed payment

can be found in our other articles.

How to earn points for pension funding?

It was said earlier that an important aspect that influences the size of the monthly pension benefit is pension points.

The amount of pension compensation generated before 2015, before the pension points system came into effect, is calculated according to previously adopted rules, taking into account length of service and monthly salary before 2002, as well as insurance contributions after 2002. The volume of received pension savings is subject to indexation annually along with the indexation of the insured pension part. The final amount is converted into points: to do this, you need to divide it by the value of one pension coefficient established on January 1, 2015 and equal to 64.10 rubles.

Every 12 months of work are valued at a certain number of points.

Starting from 2015, every 12 months of work activity will be assessed in pension points, accrued after analyzing the total amount of insurance payments made by the employer.

Through pension points, the “non-insurance” periods will be assessed. These include:

- time spent serving in the Russian Armed Forces – 1.8 points per 12 months;

- time of care of one of the parents for the first, second, third or fourth child until he turns 1.5 years old - 1.8, 3.6 and 5.4 points per year, respectively;

- the time during which care was provided for a disabled citizen of group I, a disabled child or a person who celebrated his 80th birthday - 1.8 points per 12 months;

Note! If a person has reached retirement age and decided to retire, then before assigning pension compensation to him, all earned pension points will be summed up and converted into Russian rubles.

The amount of one pension coefficient as of January 1, 2015 was 64.10 rubles. Every year this value is revised based on the decision of the Russian government. The amount of one pension coefficient as of January 1, 2018 is equal to 81.49 rubles.

The cost of one pension point increases annually

For example, a person has earned 160 points that form pension compensation. The insurance share of his pension capital will be as follows: 160 * 87.24 rubles = 13958.40 rubles + 5334.19 rubles (guaranteed payment) = 19292.59 rubles.

How to check the correctness of the accrued amount

The fastest option would be to write an application to the Pension Fund at your place of residence. In this case, the citizen must write that he asks for clarification of the calculations of the pension and its components, wants to receive information about what length of service is taken into account in the calculations, and what periods are excluded and why.

Fund employees are given a period of five days. Upon expiration, the citizen must be sent a written response. If an error is detected, pension payments will be automatically adjusted.

But, if you don’t want to visit the fund, you can check on your own at home how correctly the payments were calculated. To do this, you can use the Pension Fund calculator.

To obtain all the necessary information, you must enter information about your gender, date of birth, and length of service. They also enter information about the category of employment, write down whether he is an employee or a self-employed citizen. In addition, they indicate the salary in current prices, the duration of the non-insurance period, which includes military service, child care and other situations.

It is also worth informing whether there are plans to apply for a pension later than the deadline.

Ultimately, the calculator will show the number of points and the amount of the insurance pension, taking into account current legislation.

Reference! It is impossible to calculate a long-service pension for a military personnel who has no civilian experience using the Pension Fund calculator.

To find out how many points have been awarded, you can use the services of the State Services website. To obtain this information, indicate information about the status of your individual personal account. This information is provided free of charge. It will take no more than a few minutes to generate the report.

In addition to information about the number of points, here you can find out about the amount of total length of service, places of work, the amount of accrued wages and insurance pension contributions. The full volume of all this information has been present in the Pension Fund database since 1997. It was this year that a personalized accounting system was introduced. If you need to obtain information about earlier periods, then you will have to personally visit the territorial office of the Pension Fund of Russia.

After the pension is accrued, the citizen will receive it using postal services, a bank or special delivery companies . You can change your decision on the method of receipt, but to do this you need to send a written application to the Pension Fund.

What kind of pension compensation can a person who has never worked officially hope for?

A Russian who has never earned an official living and has not worked the required number of years can hope for a social old-age pension. The determination of such compensation is carried out 5 years later than the age pension plan. The amount of this compensation from April 1, 2018 is equal to 5957.28 rubles.

If a person has never officially earned money, he can count on a social pension

Insurance pension: who is entitled, how to apply

Let's face it: Most people don't care much about retirement. If old age is still far away, it seems like a matter of the future, which can always be postponed until later.

At the same time, everyone wants to have enough means of subsistence in old age so as to be less dependent on the vicissitudes of fate. But this can be achieved if you take the necessary measures now, without waiting for retirement age.

It is at least useful for future pensioners to understand how the pension system is structured and what nuances there are in modern legislation. The most common questions: what are funded, insurance and social pensions, what is the difference between them, how to draw up documents.

READ What to do if the appeal overturned the decision of the court of first instance: the period of consideration, how the appellate court proceeds, how to find out whether an appeal has been filed, the grounds for the appeal, the procedure for appealing, what documents are needed

In this article we will go into detail about everything you need to know about it.

Minimum pension compensation in the Russian Federation for 2021

A pensioner who does not fulfill work obligations cannot receive pension compensation of less than the regional subsistence minimum. If the pension compensation after recalculation turns out to be less, then the citizen is entitled to an additional social payment. With its help, pension compensation will reach the subsistence level.

Note! It follows from this that the minimum pension compensation for a citizen of the Russian Federation is equal to the regional subsistence level.

The pension cannot be less than the regional subsistence minimum

How to calculate an insurance pension in 2021 - calculation formula

The formula for calculating the insurance pension will not change in 2021. It will remain the same - but there are suggestions that it will change in 2025.

The standard formula for calculating pensions is:

As you may have noticed, this formula contains bonus and increasing coefficients. They will affect the amount of your pension benefit.

In addition, the benefit amount will be calculated based on the following indicators:

- Points that a citizen has earned during the year. A minimum of 18.6 points must be collected over the entire working period.

- Amount of work experience.

- Retirement period.

- Retirement age.

- Individual pension coefficient.

- The size of the fixed payment.

- Pension point value.

To calculate pension payments without bonus coefficients, you can use another formula:

SP = (PB * SB) + FV,

Where:

- SP - insurance pension.

- PB - points collected by a citizen.

- SB - the price of the ball at the time of calculation.

- FV - fixed payment.

To calculate your pension, you should take into account the following parameters when calculating:

| Year | Minimum IPC amount to receive a pension | Minimum experience | IPC - maximum amount for a year without pension savings | IPC - the maximum amount for a year with pension savings |

| 2019 | 16,2 | 10 years | 9,13 | 5,71 |

| 2020 | 18,6 | 11 years | 9,57 | 5,98 |

| 2021 | 21 | 12 years | 10 | 6.26 |

| 2022 | 23,4 | 13 years | 10 | 6,25 |

| 2023 | 25,8 | 14 years | 10 | 6,25 |

| 2024 | 28,2 | 15 years | 10 | 6,25 |

| 2026 and beyond | 30 | 15 or more years | 10 | 6,25 |

IPC in the new pension reform in Russia - the percentage of the individual pension coefficient

Additional fees

A retired citizen has the right to receive an additional supplement to the basic pension in the following cases:

- for length of service in the Far North or areas related to them;

- for persons who are dependent on a citizen (a pensioner provides for disabled persons and minors);

- for living and working in rural areas;

- if you reach the age of 80 years;

- if a citizen lives in the Far North (increased coefficient for the region);

- EDV in case of receiving payments due to disability.

Some groups of citizens receive additional payments

So, the calculation of a pension can occur differently depending on how much a person has worked, what his salary is, and whether there are any privileges. For a better understanding of the calculation, you can contact the Pension Fund or MFC branch.

Let's understand the concept

A labor or insurance pension is a monthly payment, the amount of which is determined depending on contributions to the Pension Fund for the period of working activity. The insurance period is the main condition for assigning payment.

Appointed in cases where a person loses the opportunity to earn money on his own. Loss of ability to work is possible in the event of reaching retirement age, receiving the status of a disabled person, and so on. In some cases, the generally established period for going on vacation may be reduced.